ESG Investing is here to stay

| ECube India | 5 Min Read

The Covid pandemic and growing anxiety about the adverse impact of global warming have increased public interest in Environment, Social and Governance (ESG) investing.

ESG investing strategies have been broadly summarised by the Global Sustainable Investment Alliance (GSIA) under seven broad themes: impact investing; best-in-class screening; sustainability-themed investing; norms-based screening; corporate engagement; negative screening; and ESG integration.

As of 2020, per GSIA, these strategies were used to manage assets of over $35 trillion, and according to a Bloomberg study, global ESG assets are on track to exceed $53 trillion by FY 2025.

However, the growing popularity of ESG investing has recently faced increasing criticism.

Questions have also been raised about the underwhelming performance of many ESG funds in the past year, especially when benchmarked with funds that were happy to invest in ESG-unfriendly fossil fuel companies that saw record profits in the wake of the Russia-Ukraine war.

We discuss three major critiques of ESG investing and why they should not impede its sustained growth.

Critique 1: ESG is subjective and difficult to measure, the criteria for investing are confusing, and this distracts from a pure returns focus.

There is considerable merit to the argument that ESG is hard to measure. ESG rating providers typically track several hundred parameters under each of E, S and G, and these are neither identical nor do they lend themselves to comparable scoring.

Yet, ESG investing strategies — all the seven identified above by GSIA — play a valuable role in offering investors options around how their assets might be managed. From funds that target impact in areas like healthcare, to funds that focus on backing companies that are successfully reducing their greenhouse gas footprint, to activist funds that force the pace of change in reluctant company managements, a plethora of choices are getting created for investors.

The onus of explaining and defending the benefits of each such strategy would obviously fall on the respective fund manager. Just as there is a spectrum of public market investment choices, ranging across bullish and bearish strategies, likewise, there is a spectrum of ESG outcomes promised by different fund managers, and it is up to investors to select the fund strategy that offers the most meaningful outcome to them. The outcome sought may or may not be predicated on financial returns, and this is clearly a choice entirely in the hands of the investors.

Critique 2: Business success and ESG performance are not always correlated.

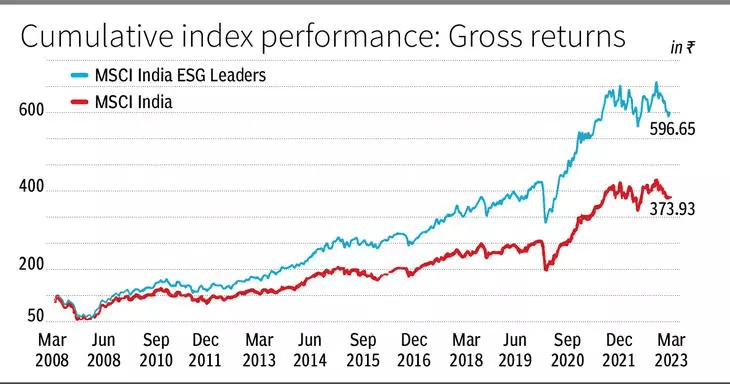

Critics question whether better ESG performance necessarily leads to better financial returns. They point to the underperformance of many ESG funds when benchmarked with market returns. This is a fair critique, and the fund managers of such ESG funds need to explain what may have gone wrong with their strategies. It is simultaneously worth noting that in markets like India, even though the ESG focus is relatively nascent, the MSCI India ESG Leaders Index has outperformed the benchmark index over various periods, including from inception, and over the past 10 and five years. (See chart)

For many fund managers, the ESG performance of companies actually offers a proxy measure for prudent risk management. A company that does a better job of managing risks relating to various ESG parameters including environmental impact, employee engagement, community support and good governance, is likely to be better able to navigate through black swan events like Covid and other looming challenges like climate change.

Plenty of research papers point to the outperformance on hard-core business and financial parameters of ESG leaders as compared to ESG laggards, across geographies.

Promised outcomes from ESG investing may or may not have much to do with a singular dimension of business success linked to financial returns. Outcomes will also depend on a variety of factors such as the tenure of investments, business cycles, geopolitical developments, and so on. And as with any investment fund, outcomes will be shaped significantly by the capability of the fund manager, and to expect that every ESG fund will be successful is unrealistic.

Critique 3: ESG investing is a gimmick.

For many critics, ESG investing represents a form of virtue signalling and is essentially a gimmick.

They point to frequent instances of greenwashing by companies to make the point that the search for strong ESG performance incentivises superficial actions without a genuine commitment to change.

However, a few bad apples cannot be the basis for rejecting an effort in the direction of improving ESG performance.

We have seen the perils of short-term thinking which led to the Great Financial Crisis. ESG investing, by focusing on certain defined ESG metrics, usually with a preference for long-term sustainable growth, can be a force for good.

As climate change worsens and more sustainability-linked challenges emerge, stakeholders will increasingly look towards reporting and disclosure frameworks for information on the issues that matter to them. ESG investing strategies will consequently resonate with many stakeholders.

In India too, we are seeing regulatory pressure moving the needle on this front. SEBI is tasking ESG funds to improve their corporate engagement and stewardship protocols.

Likewise, the RBI is also beginning to press banks and lending institutions to incorporate an assessment of both physical and transition risks across a range of climate-related scenarios, and to determine their resilience to financial losses; for risk mitigation, it wants them to encourage their customers to be more responsible and provide relevant climate-related disclosures, and where required, adopt steps like reducing the tenor of loans to customers who may face higher climate risks, or persuading them to take on insurance against extreme weather and embrace a clean energy transition strategy.

The message is clear. ESG investing is here to stay, and rumours of its imminent demise are completely unfounded.